There’s no shortage of high-yield stocks on the market, and it’s not difficult to find them, but which ones better reflect your investing outlook? If you share my opinion, the outlook remains positive for energy prices, and the U.S. housing market will recover in time. Devon Energy (NYSE: DVN) and Whirlpool (NYSE: WHR) are great buys right now. However, despite being an exciting investing proposition in its own right, 3M (NYSE: MMM) is not the stock high-yield investors should be buying. Here’s why.

Devon Energy (trailing dividend yield of 5%)

Devon Energy pays a fixed-plus-variable dividend, using the remaining free cash flow after the fixed dividend (currently $0.22 a quarter) is paid and share buybacks are completed.

It’s a flexible strategy. When management feels its stock is undervalued, it prioritizes share buybacks. For example, in the fourth quarter of 2023, management retired 5.2 million shares for $234 million, paid a fixed dividend of $0.20 per share for $127 million, and paid a variable dividend of $0.22 per share using $140 million.

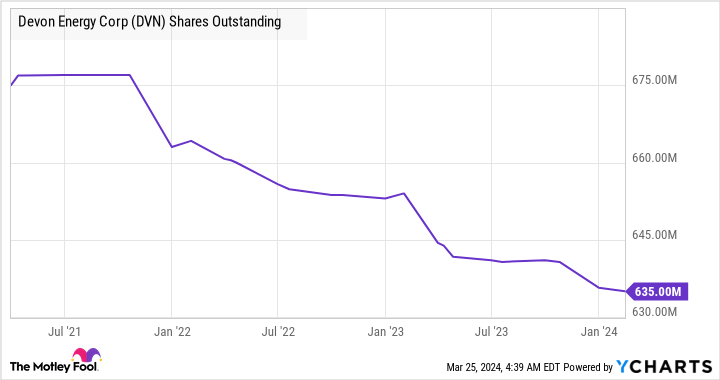

The chart below shows Devon has a pretty good track record of reducing its share count. High-yield investors should welcome this as it increases the share of their claim on future cash flows from Devon Energy.

Devon also has a good track record of growing resources, not least through extensions and discoveries.

By my calculations, based on a price of oil of $80 per barrel in management’s 2024 projections and the current share price of $48.37, Devon’s free-cash-flow (FCF) yield could be almost 10% in 2024. Given that management is targeting to return 70% of FCF to investors in 2024, there should be ample room to pay a hefty dividend as well as buying back shares to enhance the dividend per share in the future.

While it’s not clear what the variable dividend will be in 2024, at the current price of oil, Devon has plenty of potential to pay a substantial dividend this year.

Whirlpool for a housing recovery and its 6.3% dividend yield

It won’t be a vintage year for Whirlpool in terms of its headline numbers. Over an extended period, relatively high interest rates are slowing the housing market and putting pressure on household appliance sales. Given that existing home sales drive 25% of U.S. demand for appliances, and 15% comes from new home sales, it’s no surprise to learn that Whirlpool expects its 2024 comparable sales to be flat with 2023 at $16.9 billion, with its earnings before interest and taxation (EBIT) margin also flat for 2023 at 6.8%.

There’s very little Whirlpool can do about its end markets, but it can change where it focuses on operating. That’s exactly what management is doing by agreeing to transfer its major European domestic appliances business to Arcelik’s European business while obtaining a 25% stake in the new company. It’s a good move, as Whirlpool’s European business has bled cash in eight of the last 15 years and had an EBIT margin of just 1.8% in 2023.

As such, Whirlpool will focus more on its core North American market, which is on track to generate a 9% EBIT margin in 2024. In addition, management’s cost-cutting measures took $800 million out of costs in 2023, and it plans to take $300 million to $400 million out in 2024. These actions should set Whirlpool up nicely to benefit from a lower interest rate in North America in the future.

Don’t buy 3M for its 5.7% dividend yield

There is a value case for buying 3M stock, not least as management’s restructuring actions hopefully turn around its lackluster margin performance in recent years. In addition, there are some signs of improvement in some of its key end markets, such as consumer electronics, semiconductors, and electronics.

That said, the spinoff of its healthcare business, Solventum, will take away a valuable source of reliable cash flows. Moreover, 3M continues to face significant legal costs as it deals with litigation issues and will have multibillion-dollar annual cash calls from legal settlements.

On the other hand, 3M will receive $7.7 billion in proceeds from the Solventum spinoff and will retain a 19.9% stake in the healthcare business, which it can sell off to raise cash. The bottom line is that 3M can maintain its dividend at the current level, but using cash to restructure an ailing company might not be the best use of shareholders’ money.

Finally, 3M’s current CEO, Michael Roman (who will become executive chairman on May 1), has fallen short of explicitly confirming the dividend will be maintained at the current level after the Solventum spinoff, but has promised “an attractive dividend.”

Therefore, don’t be surprised if 3M cuts its dividend in 2024.

Should you invest $1,000 in 3M right now?

Before you buy stock in 3M, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and 3M wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of March 25, 2024

Lee Samaha has no position in any of the stocks mentioned. The Motley Fool recommends 3M. The Motley Fool has a disclosure policy.

2 Ultra-High-Yield Stocks to Buy Hand Over Fist and 1 to Avoid was originally published by The Motley Fool

feed from Finance.yahoo.com