Artificial intelligence (AI) has been the prevailing growth theme in the market since ChatGPT hit 100 million monthly active users in January 2023.There’s been plenty of discussion of the companies supporting AI, but what’s talked about less are the companies successfully investing in AI and monetizing it.

Here’s why Meta Platforms (NASDAQ: META), UiPath (NYSE: PATH), and Trimble (NASDAQ: TRMB) are three AI stocks worth considering now.

Meta is leveling up with AI

Daniel Foelber (Meta Platforms): Chip giants like Nvidia provide the processing backbone needed to run complex AI models. While the semiconductor industry has been front and center of the AI growth narrative, the whole story falls apart if companies aren’t monetizing AI.

It’s one thing to invest in AI and another to make money from it. Meta Platforms is one of the best and most easily understandable examples of what successful AI investment looks like.

Social media apps make money on advertising, and advertisers want to see high user engagement and targeted messaging. An ad does little good if it reaches the wrong audience and people don’t regularly visit the platform.

Instagram Reels is an excellent example of how Meta has leveraged AI in a short amount of time. It wasn’t long ago that Meta stock reached a multiyear low as TikTok posed an existential threat. Meta came out with its short video counter Reels to combat TikTok. Reels was announced in August 2020 but wasn’t a big success right off the bat.

For Reels to supplement TikTok, Meta had to keep users engaged with content they liked. This algorithm was far more complex than classic Instagram, which was more about a user choosing who they wanted to follow and then viewing recently posted content simply by who they followed. Reels focused on preferences, rather than a linear timeline.

Meta is investing heavily in making its platforms more engaging for users. However, the other side of the equation is equally important — giving advertisers and content creators the tools they need to boost messaging. To quote CEO Mark Zuckerberg from Meta’s Q4 2023 earnings call:

Now moving forward, a major goal, we’ll be building the most popular and most advanced AI products and services. And if we succeed, everyone who uses our services will have a world-class AI assistant to help get things done, every creator will have an AI that their community can engage with, every business will have an AI that their customers can interact with to buy goods and get support, and every developer will have a state-of-the-art open-source model to build with.

These investments come at a high price. Meta spends the most on research and development (R&D), by far, relative to its revenue, than the major tech stocks. Based on trailing-12-month data, Meta is allocating over $0.28 of every dollar in sales toward R&D. But so far, it has more than justified that spending.

With a 24.3 forward price-to-earnings ratio, Meta is surprisingly affordable for a stock that’s up 150% over the last year and is crushing the market year to date.

UiPath helps other businesses work smarter with artificial intelligence

Scott Levine (UiPath): Soaring almost 43% over the past year, UiPath stock has given investors a lot to celebrate. The company, a leader in business automation solutions, may not have the name recognition like other AI specialists, but that doesn’t mean investors haven’t celebrated the company’s accomplishments. UiPath recently reported strong fourth-quarter 2024 financial results and provided an encouraging outlook for fiscal 2025.

From healthcare to manufacturing to insurance, UiPath helps customers in various industries increase productivity and efficiency by offering automation solutions. For software companies such as UiPath, one valuable way to assess a company’s performance is through the annual recurring revenue (ARR) metric.

UiPath defines this as its ability “to acquire new subscription customers and to maintain and expand our relationships with existing subscription customers.” Looking at the company’s fourth-quarter 2024 financial results, it seems that UiPath is excelling, ending fiscal 2024 with $1.46 of ARR — a 22% year-over-year increase. Management expects further growth in 2025, forecasting ARR of $1.725 billion to $1.730 billion.

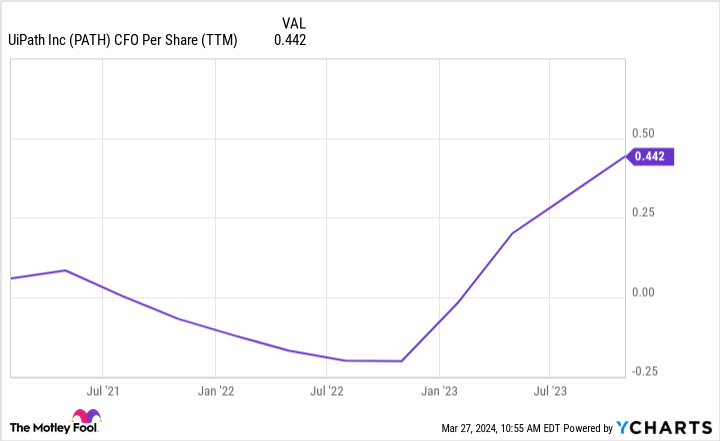

Another auspicious sign for UiPath is its growing cash flow. While revenue growth is great, it means little if the company isn’t able to translate its sales to cash — something that it has been steadily doing for more than a year.

Management also expects its cash flow to improve in fiscal 2025. It forecasts that adjusted free cash flow will grow from $309 million in fiscal 2024 to $350 million in fiscal 2025.

Trimble’s growth is just getting started

Lee Samaha (Trimble): At the heart of the AI revolutions lies the idea that massive amounts of data can generate ongoing actionable insights to improve real-time decision-making. That argument neatly defines the investment case for buying Trimble stock.

The industrial technology company’s origins are in highly precise positioning hardware used in navigation systems. Still, its future lies in combining that hardware with software and services that analyze and model data and help improve its customers’ daily workflows.

For example, construction/infrastructure projects can be precisely managed to help reduce waste and the cost/time overruns that the industry is notorious for. Architects and planners can improve the design and planning of buildings/projects. Furthermore, projects can be better maintained using AI data analysis to more accurately predict potential issues.

Trucking fleet routes can be optimized in transportation to help reduce fuel costs and improve schedules. Farmers can make more informed decisions and precisely plan planting, nurturing, and harvesting in agriculture. In geospatial, Trimble’s solutions can aid urban and infrastructure planning.

The shift to relatively more software and services revenue is improving Trimble’s profit margins and cash-flow generation and will likely create significant value for shareholders. While some of its end markets remain challenged in 2024, Trimble continues to grow its underlying recurring revenue at a double-digit rate, and the future remains bright for the company.

Should you invest $1,000 in Meta Platforms right now?

Before you buy stock in Meta Platforms, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Meta Platforms wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of March 25, 2024

Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Daniel Foelber has no position in any of the stocks mentioned. Lee Samaha has no position in any of the stocks mentioned. Scott Levine has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Meta Platforms and UiPath. The Motley Fool recommends Trimble. The Motley Fool has a disclosure policy.

3 Scorching Hot Growth Stocks That Are Capitalizing on AI was originally published by The Motley Fool

feed from Finance.yahoo.com