Welcome to the forefront of the artificial intelligence (AI) revolution, where transforming the mundane into the extraordinary is just another day at the office. Three Motley Fool contributors, each with a keen eye on the AI landscape, put their heads together to share their best AI investment recommendations as March rolls over into April.

It’s quite the lineup. UiPath (NYSE: PATH) makes the routine remarkable. Chips from Nvidia (NASDAQ: NVDA) are training your favorite AI platforms right now. And Broadcom (NASDAQ: AVGO) is crafting the world’s AI infrastructure, one networking chip at a time.

How UiPath stands out in the AI market

Anders Bylund (UiPath): Business automation expert UiPath’s place in the world is quite simple. By automating the simple, mundane, and repetitive tasks in a company’s daily operations, employees can focus their efforts on innovative and value-added functions instead.

After applying UiPath’s AI-driven bots to their daily grind of uninspiring jobs, clients tend to save costs and speed up basic processes. With a newfound freedom to pursue more-fulfilling projects, their employees become happier and more effective.

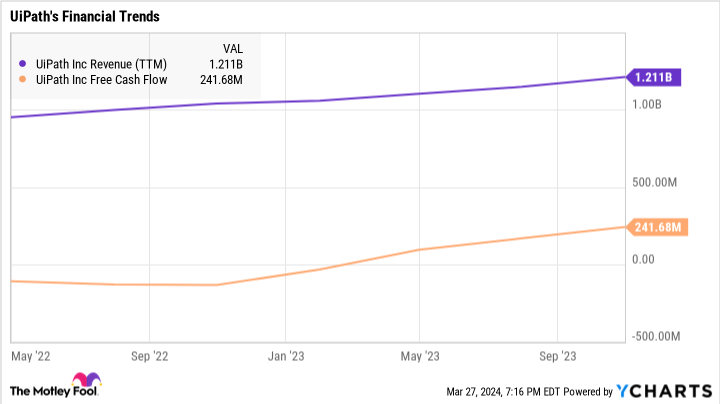

So it’s no surprise to see UiPath’s business booming in the ongoing AI boom. Sales rose 31% year over year in the recently published fourth-quarter report. Free cash flows were essentially break-even in the 2023 fiscal year that ended Jan. 31, 2023, just a few weeks after OpenAI’s ChatGPT introduction. One year later, for the 2024 fiscal year, UiPath had collected $309 million of free cash flow on $1.3 billion in top-line revenue. In other words, the public frenzy for AI tools boosted the company’s cash-based profit margin from zero to 24% in just one year.

This should be the start of a sustained growth spurt. AI tools are an easy sale right now, and the company enjoys strong word-of-mouth marketing when new customers walk away happier and richer.

But nobody has spread the word across Wall Street yet. UiPath trades at 10 times sales and 34 times forward earnings estimates. These ratios would be appropriate for a moderately growing retailer or basic-materials producer. For a high-margin software expert with skyrocketing sales, they look like a bargain.

So if you’re looking for a modestly priced AI stock with a generous shot of nitro in its sales-growth engines, UiPath deserves a second look. This bargain is hard to beat, even if you pointed UiPath’s own automation tools at the problem. Cathie Wood is buying the stock hand over fist these days, and you should consider following her lead.

Broadcom: Now much more than just another chip supplier

Billy Duberstein (Broadcom): Even though it’s had a massive run, Broadcom might still be underrated as an AI juggernaut.

The stock trades at 28 times this year’s earnings estimates, but the company has been a regular beater of analyst estimates, so it’s a pretty good bet that Broadcom beats earnings estimates this year as well. That’s especially true because its two AI chip divisions seem poised for strong growth.

Broadcom’s first AI chip segment involves merchant-networking chips, where Broadcom leads in ethernet communications through its Tomahawk switching chips, Jericho routing chips, as well as optical transceiver chips that all work together in enabling lightning-fast communications.

The second AI division makes custom ASIC chips that combine with customers’ IP to form custom AI accelerators for specific uses. For instance, Alphabet uses Broadcom’s IP in its custom Tensor Processing Units, and Meta Platforms is a second key customer. These two mega-clients each bring in lots of money for Broadcom, especially over the past year as AI applications have taken off.

Recently, Broadcom increased its outlook for AI chip sales growth in 2024, forecasting AI revenue to reach 35% of its semiconductor revenue this year while amounting to over $10 billion in total. That’s up from a 25% proportion that it had forecast in its prior quarter.

Not only that, but since the earnings release, Broadcom announced a third ASIC customer, which is no doubt a large tech company set to grow a lot in the coming years. So its AI revenue could even exceed what management had forecast on its recent earnings report.

Yet while the AI chip segment is booming, Broadcom also disclosed exciting news regarding its software segment, which has grown substantially with the acquisition of VMware last November.

With that acquisition, software makes up nearly half of Broadcom’s revenue. But it also appears the VMware business could be inflecting on a stand-alone basis — conveniently for shareholders, just after Broadcom closed the purchase. On a recent conference call with analysts, CEO Hock Tan said he sees VMware growing by double digits sequentially each quarter through this year.

That would be a serious acceleration relative to VMware’s pre-acquisition growth, reflecting increased pricing for the new VMware Cloud Foundation product. This premium product is an integrated software stack that virtualizes all aspects of a customer’s computing, storage, networking, and even AI GPUs in their on-premise data centers. Hardware virtualization is the process of creating virtual versions of physical desktops and operating systems — its benefits include better performance and lower costs.

In a new AI world, it’s likely that corporate customers will operate between on-premise data centers and public clouds, depending on the capabilities of each. And it’s also likely that companies will want to use cloud-based AI tools but will also be wary of sharing their data outside their own on-premises data centers. In that world, VMware should be even more valuable as the connective tissue between all these computing environments.

But perhaps the larger point is that Broadcom is now more than just a chipmaker. As the only tech platform with a roughly 50/50 split between chips and software, it can now look in both the hardware and software world for future acquisitions. Given that the company’s business model is centered around acquisitions, investors might not realize how much its growth prospects have increased with the VMware buy.

As such, despite being up 116% over the past year, Broadcom stock looks like it might still be underrated relative to other AI darlings.

Are we closer to peak Nvidia than investors believe?

Nicholas Rossolillo (Nvidia): Nvidia has had meteoric rises in the past, but this one from the last two years takes the cake. As the superpower responsible for kicking off the AI race, Nvidia’s name (rooted in the Latin “invidia” for envy, the feeling the co-founders, including CEO Jensen Huang, wanted to inspire among competitors) has become a self-fulfilled prophecy as the semiconductor industry and tech sector at large have fallen into the company’s orbit.

Of course, we’re far away from Nvidia leading the field in graphics processing alone. The company’s GPUs have become the backbone of new generative-AI training, and for a lot of AI inference, too (once the AI system has been trained and is put to use).

Huang recently said that his company is at the forefront of two giant markets. The first is the massive task of upgrading the world’s existing data center fleet to accelerated computing hardware. And the second is the new generative-AI market that needs brand-new purpose-built data centers.

The generative-AI market, geared especially toward AI training, is already dominated by Nvidia. Its total value is yet unknown, but could be worth hundreds of billions of dollars in total data-center assets within the next few years.

The existing global data-center market is currently valued at $1 trillion. The hardware within this massive computing footprint tends to get upgraded every four to five years. And right now, the upgrades needed are accelerated computing — precisely the type of chips that Nvidia has become synonymous with.

Paired with the new generative-AI infrastructure being installed, this existing data-center upgrade cycle is why one of Nvidia’s chief rivals, AMD (NASDAQ: AMD), has said total sales of accelerated-computing chips could reach $400 billion in 2027.

Given Nvidia’s absolute dominance up to this point, this gargantuan opportunity is why the company now fetches an absurd-looking $2.3 trillion market cap — or 37 times current-year expected earnings per share. This ranks Nvidia as one of the world’s most highly valued companies (one of the “Magnificent Seven”), even though its actual revenue and profit are still far behind that of the largest businesses. Investors believe Nvidia will remain in high-growth mode for quite some time.

And grow it will. Management provided early guidance that assumes another year of massive growth in 2024. For reference, the consensus from Wall Street analysts is now at least 80% revenue expansion this year, with profit margins remaining near all-time highs.

Given these assumptions, investors who don’t already own Nvidia should tread cautiously. Its business is cyclical, and at some point, the AI-infrastructure construction frenzy will moderate and go through a cyclical decline. But are we close to peak Nvidia sales? It certainly doesn’t look like it.

Should you invest $1,000 in Nvidia right now?

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than tripled the return of S&P 500 since 2002*.

*Stock Advisor returns as of March 25, 2024

Randi Zuckerberg, a former director of market development and spokeswoman for Facebook and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Fool’s board of directors. Suzanne Frey, an executive at Alphabet, is a member of The Motley Fool’s board of directors. Anders Bylund has positions in Alphabet and Nvidia. Billy Duberstein has positions in Alphabet, Broadcom, and Meta Platforms. His clients may own shares of the companies mentioned. Nicholas Rossolillo has positions in Advanced Micro Devices, Alphabet, Broadcom, Meta Platforms, Nvidia, and UiPath. The Motley Fool has positions in and recommends Advanced Micro Devices, Alphabet, Meta Platforms, Nvidia, and UiPath. The Motley Fool recommends Broadcom. The Motley Fool has a disclosure policy.

From Silicon to Software: A Quick and Easy Guide to AI Investing This Spring was originally published by The Motley Fool

feed from Finance.yahoo.com